Market Color | Opening Gambit–June 16,2025

Markets on Edge: Geopolitics Ignites Volatility.

Hello Metamacro readers! Cheer to the new week

The financial world reeled this past week as escalating tensions in the Middle East, specifically an Israeli airstrike on Iran, sent shockwaves through global markets, abruptly ending a promising rally. Equities plunged, and oil prices soared, underscoring the fragility of the current economic landscape.

Weekly Market Wrap-Up: Geopolitical Tensions & Tech Swings Dominate Volatile Week

Wall Street experienced a turbulent week, with initial optimism over trade talks and AI innovations giving way to a sharp sell-off driven by escalating geopolitical tensions in the Middle East. While the S&P 500, Nasdaq, and Dow Jones initially posted gains, the market’s direction reversed dramatically by week's end.

Tech Undercurrents: Tech giants presented a mixed bag. Alphabet rallied on the back of strong AI advancements, while Microsoft, despite robust market performance, saw some slippage. Apple disappointed investors with vague AI announcements at WWDC, contrasting sharply with Tesla's surge fueled by its robotaxi rollout momentum. GameStop's earnings beat profit expectations but missed revenue forecasts, eliciting varied market reactions. Oracle was a standout, soaring to a new record high driven by strong demand for its AI-powered cloud services.

Global Dynamics Shift: U.S.-China trade negotiations saw a significant restructuring of the Geneva agreement. China pledged upfront rare earth materials crucial for U.S. industries, in exchange for continued access for Chinese students to U.S. universities. The U.S. maintained its existing 55% tariff structure on Chinese imports. Meanwhile, OPEC+'s struggle to meet production forecasts kept oil prices elevated, and a U.S.-Mexico deal to lift steel tariffs appeared imminent.

Economic Picture & Inflation Relief: The latest Consumer Price Index (CPI) report brought some relief, showing inflation cooling below expectations. Headline CPI rose 2.4% year-over-year, and core CPI increased 2.8%, both softer than anticipated. This disinflationary trend eased fears of tariff-driven price hikes. However, the U.S. April jobs report presented a mixed picture, with accelerating wage growth but declining full-time employment and labor participation. Consumer sentiment for June, as measured by the University of Michigan survey, is anticipated to provide further insights into economic perceptions.

Market Jitters from Middle East & Aviation Concerns: The week concluded with significant market volatility following Israel's preemptive airstrikes on Iran, which sent shockwaves across global financial markets. This major escalation in Middle East tensions triggered a broad risk-off sentiment, causing U.S. stock futures (Dow, S&P 500, Nasdaq 100) to tumble sharply. Oil prices surged over 10% on fears of supply disruptions from the region, while gold, a traditional safe haven, climbed. Adding to the unease, Boeing shares dropped over 4% after an Air India 787 Dreamliner crash marked the model's first fatal incident, raising safety concerns for the aerospace giant.

Trump's Tariff Deadline Looms: All Options on the Table as July 9 Approaches

As the July 9 expiration of the 90-day pause on President Trump's "Liberation Day" tariffs draws near, the administration is signaling a wide range of potential outcomes. President Trump and his officials offered varied scenarios last week, underscoring the fluidity of the ongoing trade negotiations.

Trump himself confirmed his openness to diverse resolutions, stating Wednesday evening that he intends to issue "take it or leave it" letters to nations involved. However, he also acknowledged the possibility of extending some deadlines and expressed confidence in progress on other deals, indicating that "We're rocking in terms of deals." This suggests a multifaceted approach as the critical deadline approaches.

Middle East Tensions Derail Market Rally: Equities Retreat, Oil Surges in Volatile Week

The robust stock market rally experienced a sharp reversal this week, as escalating geopolitical tensions in the Middle East, specifically an Israeli airstrike on Iran, sent ripples across global financial markets. The incident triggered a significant surge in oil prices and prompted a broad retreat in equity markets, putting a decisive end to what had been a period of strong gains for the first full trading week of June.

By week's close, major U.S. indices recorded notable declines. The S&P 500, a broad gauge of market performance, shed 0.6% of its value. The technology-heavy Nasdaq Composite experienced a more pronounced slide, falling 1%. Meanwhile, the Dow Jones Industrial Average, representing a basket of 30 large, publicly traded U.S. companies, saw the steepest decline, dropping 1.3%. This synchronized downturn underscored investors' immediate reaction to the heightened uncertainty and potential for broader economic disruption stemming from the escalating conflict. The sudden shift reflects a classic "risk-off" sentiment, as investors moved away from equities and into perceived safe-haven assets, while commodity markets reacted directly to potential supply chain vulnerabilities.

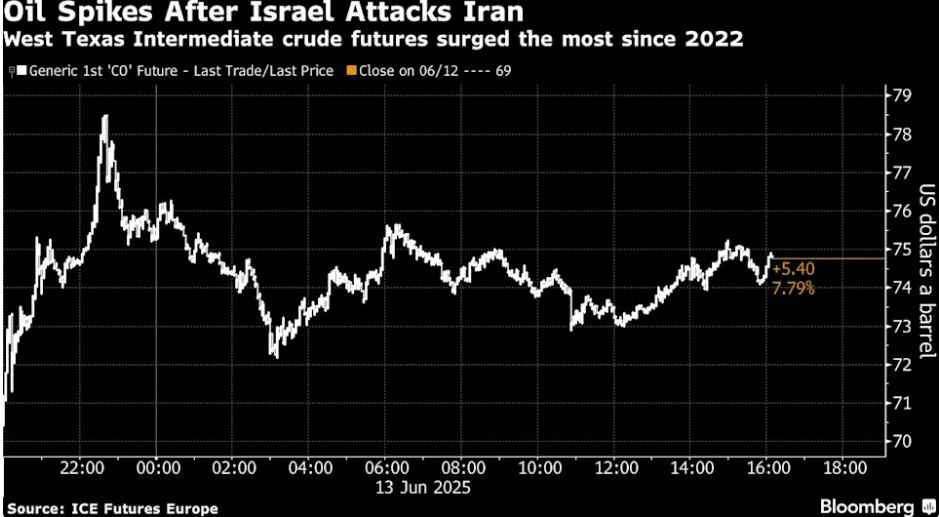

Oil Markets Erupt: Brent and WTI Soar Over 12% Amid Escalating Middle East Tensions

Global oil prices experienced a dramatic surge on Friday, culminating in significant weekly gains, as investors reacted to the escalating conflict between Israel and Iran. The direct impact of the Israeli missile launch on Iran sent a clear signal of heightened geopolitical risk, immediately translating into a substantial rally in crude benchmarks.

By the close of trading, Brent crude futures, the international benchmark, surged to just under $74 a barrel. Simultaneously, West Texas Intermediate (WTI) futures, the U.S. benchmark, changed hands at nearly $73 a barrel. This explosive movement capped off an exceptionally volatile week for energy markets, with both Brent and WTI recording gains of approximately 12% or more over the five trading days.

The pervasive concern now gripping market participants is the potential for further escalation in the Middle East. Any deepening of the conflict could severely impact global oil supplies, pushing prices even higher from their already elevated levels. Such a scenario would inevitably exacerbate inflationary pressures worldwide, posing a significant challenge for central banks and potentially weighing heavily on global economic growth. The rapid ascent in oil prices underscores the sensitivity of energy markets to geopolitical instability and the far-reaching implications for the broader economy.

Nippon Steel's US Steel Acquisition Clears Hurdle with Conditional US Approval

Nippon Steel Corp. has secured conditional approval from the United States for its ambitious $14.1 billion acquisition of United States Steel Corp. This significant development marks a pivotal moment in the protracted saga of a merger set to forge one of the world's largest steel producers.

On Friday, both companies confirmed they have formally committed to a national security agreement proposed by the Trump administration, a crucial step that has now paved the way for the deal's progression.

As part of the $55-per-share agreement, the Japanese steel giant has pledged substantial future investments in the U.S. operations. Nippon Steel will inject an additional $11 billion by 2028, which includes an initial commitment towards a "greenfield" project ,a new, entirely new facility slated for completion after 2028. This commitment reflects an increased investment from earlier pledges, made in a concerted effort to gain the necessary approval, particularly from President Donald Trump.

Furthermore, sources indicate that Nippon Steel plans to allocate an additional $3 billion beyond 2028 for the construction of another new steel mill. This would bring the total additional investment, distinct from the $14.1 billion purchase price, to an impressive $14 billion, underscoring Nippon Steel's long-term commitment to enhancing U.S. steel production capabilities.

Japan and US Intensify Trade Talks Amid Tariff Standoff and Mideast Concerns

Japan's Foreign Minister announced today that during a recent call, the Japanese Prime Minister reiterated Japan's stance on proposed U.S. tariff measures to President Trump. The leaders concluded their discussion by agreeing to accelerate ministerial-level consultations, aiming to achieve a mutually beneficial trade agreement. This diplomatic push comes as the Trump administration continues to press Japan to increase tariffs on automotive and other imports from Japan, while simultaneously urging Japan to open its economy further to a wider range of U.S. goods. A key challenge in these negotiations lies in the fundamental economic differences between the two nations: Japan's high savings rate contrasts with the U.S.'s consumption-driven economy, complicating efforts to balance trade flows.

Chinese Consumers Rebound as Retail Sales Hit Post-2023 High

Driven by government subsidies, China's retail sales in May experienced their most rapid growth since late 2023, with a notable 6.4% year-on-year increase, according to data released by the National Bureau of Statistics on Monday. This boost in domestic consumption was complemented by a temporary easing in the export sector. A tariff agreement between Beijing and Washington in mid-May provided a short-term reprieve for Chinese exporters, leading some companies to expedite shipments and intensify efforts in exploring new markets.

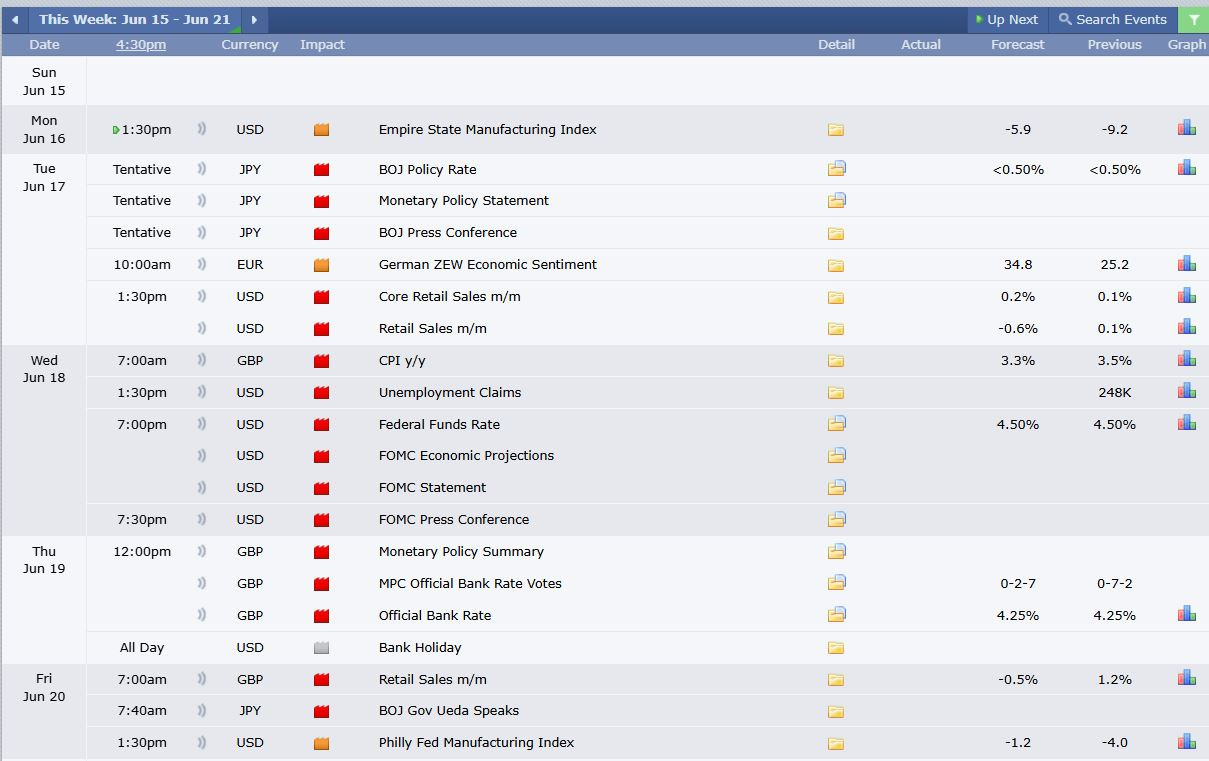

Economic Calendar

This week is all about monetary policy decisions from major central banks. It kicks off on Tuesday with the Bank of Japan (BOJ). Then, on Wednesday, the Federal Reserve will announce its latest policy. Finally, the Bank of England (BOE) will conclude its meeting on Thursday.

Beyond the central bank announcements, keep an eye on these important economic data points:

Tuesday: We'll get insights into US consumer spending with the US retail sales figures.

Wednesday: Brace for the UK CPI report, which will shed light on inflation in the UK, and US unemployment claims.

Friday: The week wraps up with the release of UK retail sales data.

Just a heads-up, Thursday is also a US bank holiday.

Earning Calendar

This week is a fairly uneventful week for earning reports but we expect earnings report from Lennar, Accenture Plc, Kroger and Darden Restaurants.

Equities Color

S&P 500 Index(SPX)

The S&P 500 index concluded the week on a downbeat note, shedding 68.29 points to close at 5976.96. This decline was largely attributed to a significant escalation of geopolitical tensions in the Middle East, specifically an Israeli airstrike on Iran.

Dow Jones Industrial Average Index(DJI)

The Dow Jones Industrial Average ended the week significantly lower, dropping 769.83 points to close at 42,203.25. This downturn was primarily driven by a sharp increase in geopolitical tensions in the Middle East, following an Israeli airstrike on Iran.

US 100 Index(NDQ)

The NASDAQ closed the week notably lower, falling 255.66 points to 21,631.03. This decline was mainly caused by a significant rise in geopolitical tensions in the Middle East, specifically after an Israeli airstrike on Iran.

FX SNAPSHOT

For the trading week, the USD was lower against the major currencies:

EUR -1.79%

GBP -0.26%

JPY -0.53%

CHF -1.26%

CAD -0.70%

AUD unchanged

NZD -0.06%

FINAL THOUGHTS

As the dust settles on a volatile week driven by Middle East tensions, the immediate future for global markets remains shrouded in uncertainty. The synchronized downturn in major indices, coupled with a dramatic surge in oil prices, vividly illustrates the profound impact of geopolitical shocks.

Content on this site is for informational purposes only and does not constitute investment advice or a solicitation to buy or sell any financial instruments. MetaMacro makes no guarantees regarding the accuracy or completeness of the information provided. Unauthorized use, redistribution, or access to proprietary content is strictly prohibited. All information is subject to change without notice. Investments involve risk, including the potential loss of principal.

— Oghenetega

MetaMacro