Market Color | Opening Gambit-July 7, 2025

Wall Street Hits New Highs on Tax Cuts and AI Boom as Trump's Tariff Deadline Puts Global Trade on Edge.

Hello Metamacro Readers!

Wall Street delivered a powerful, record-setting performance last week, as a potent combination of domestic policy victories and a "Goldilocks" jobs report fueled investor optimism. The S&P 500 and Nasdaq surged to new all-time highs on the back of a resilient labor market, the official signing of President Trump's massive tax-cut bill, and an unrelenting boom in AI stocks that saw Nvidia briefly crowned the world's most valuable company.

President Trump Signs Tax Bill Into Law

On Friday, July 4th, President Donald Trump officially signed the "One Big, Beautiful Bill" into law. The act makes the 2017 individual tax cuts permanent and introduces a range of other tax and spending measures. While the market had already celebrated its passage during the prior week's rally, the signing formalizes the new fiscal policy.

US Trading Partners Scramble for Deals as Trump's July 9 Tariff Deadline Looms

The clock is ticking for U.S. trading partners as President Trump's July 9 deadline approaches, after which he plans to impose a range of new tariffs on countries that have not secured a trade deal. President Trump confirmed his administration is shifting to a new strategy of issuing "tariff notification letters" that will bypass lengthy negotiations. These letters, set to go out in batches starting last Friday, will detail specific tariff rates ranging from 10% to as high as 70%, which are slated to take effect on August 1.

While Treasury Secretary Scott Bessent anticipates a "flurry" of last-minute agreements, the status of negotiations varies widely among key partners:

Canada: In a significant breakthrough, Canada has scrapped its controversial digital services tax, prompting the resumption of trade talks that were recently terminated. The two nations are now aiming to secure a deal by mid-July.

China: Tensions continue to de-escalate, with the U.S. easing export restrictions on chip design software and ethane. This move follows a framework agreement reached in May and signals progress toward a broader trade pact.

European Union: The EU has indicated it could accept a 10% universal tariff but is pushing for crucial exemptions for products like pharmaceuticals, semiconductors, and aircraft. Talks with the U.S. were expected to continue through the weekend.

Vietnam: A deal has already been reached. Vietnamese imports will face a 20% tariff, while a higher 40% tariff will target goods transshipped from China. In return, many U.S. goods will receive duty-free access to Vietnam.

Japan: Negotiations have soured significantly. President Trump has signaled he will impose tariffs of 30-35% on Japanese goods, stating that Japan has been "very tough" and "spoiled" in the talks.

South Korea: Facing the deadline, South Korea is actively seeking an extension and held talks with the U.S. Trade Representative over the weekend, proposing manufacturing partnerships in exchange for reduced tariffs on key exports like cars and steel.

OPEC+ to Boost August Oil Output by 548,000 Barrels Per Day

OPEC+ has decided to accelerate its oil production increases, agreeing on Saturday to boost output by 548,000 barrels per day for the month of August. This decision marks the group's first meeting since recent Middle East tensions caused a spike and subsequent fall in oil prices.

The August increase, which is larger than the 411,000 bpd boosts seen in May, June, and July, will be shouldered by eight members, including Saudi Arabia and Russia. Citing a stable global economic outlook and low oil inventories, the alliance is continuing to unwind a voluntary 2.2 million bpd cut it began reversing in April.

With this latest hike, OPEC+ will have returned over 1.9 million bpd to the market, leaving just 280,000 bpd of that specific cut remaining. The group, which still has other deeper cuts of 3.66 million bpd in place, will meet again on August 3rd to determine its next steps.

Economic Calendar

The upcoming week features a relatively sparse economic calendar, with the primary data releases of note being the U.S. weekly employment claims and the United Kingdom's month-over-month GDP report.

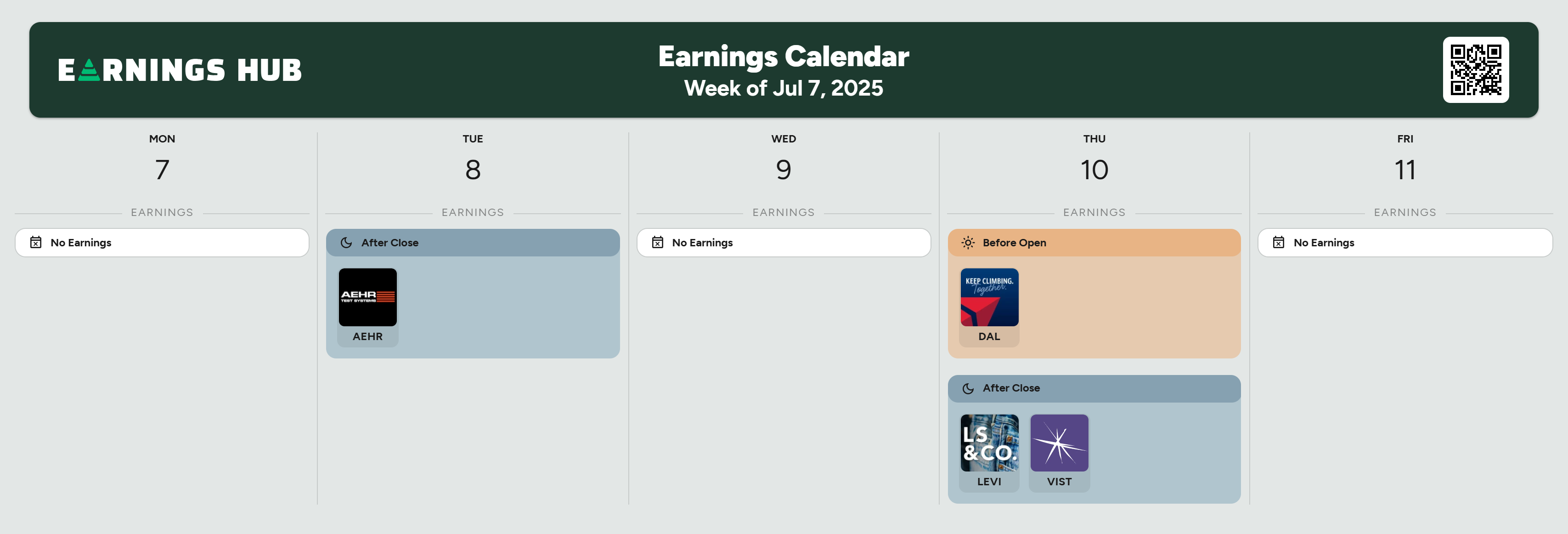

Earning Calendar

The week is set to have a very quiet start, confirming that the second-quarter earnings season will begin slowly before picking up steam.

Aehr Test Systems: A semiconductor equipment company, its results will provide an early look into the demand and capital spending within the semiconductor industry, a sector that has been at the heart of the market's AI-driven rally.

Delta Air Lines: As one of the first major airlines to report, Delta's earnings are a crucial economic bellwether. Investors will be watching closely for commentary on summer travel demand, booking trends, and the impact of fuel costs, all of which provide vital signs about the health of the consumer.

Levi Strauss & Co: The iconic apparel maker's report will offer insights into consumer discretionary spending and the state of the retail sector. Its performance can indicate how willing households are to spend on non-essential goods.

Vistra Corp: This report will be a key focus for a major emerging market theme. As a large-scale power producer, Vistra has been a top performer due to the "AI Energy Trade." Its earnings and forward guidance will be heavily scrutinized for hard data on how much the immense electricity demand from new AI data centers is translating into higher profits and long-term contracts.

Equities Color

S&P 500 Index(SPX)

The S&P 500 charged to new all-time highs, closing the week at 6,279.36. The rally was broad-based, benefiting from strength in both cyclical sectors, which rise with economic optimism, and its heavyweight technology components. The "soft landing" narrative emboldened investors to buy into a wide range of industries, from financials to industrials. The ongoing AI boom, centered on Nvidia, also provided a massive lift given the significant weighting of tech in the index.

Dow Jones Industrial Average Index(DJI)

The Dow was the week's top performer, closing at 44,828.53 and finishing just shy of its own record. As a barometer for the more traditional, industrial side of the U.S. economy, the 30-stock index surged on the news that a recession was not imminent. Companies in manufacturing, finance, and consumer discretionary rallied on the combination of a resilient labor market and the promise of tax-cut-fueled consumer spending.

US 100 Index(NDQ)

The Nasdaq continued its stellar 2025 run, closing at a new record of 20,601.10. The week's performance was unequivocally dominated by the artificial intelligence theme. Nvidia had a historic week, briefly becoming the most valuable company in the world. This tidal wave of investment lifted the entire semiconductor and big-tech ecosystem. While other growth stocks also benefited from the prospect of eventual Fed rate cuts, the sheer gravitational pull of the AI infrastructure build-out was the defining characteristic of the Nasdaq's week.

FX SNAPSHOT

The US Dollar posted a strong performance last week, with its gains accelerating significantly after the release of key U.S. labor market data on Thursday. The week's trading was defined by the theme of U.S. economic exceptionalism, which bolstered the dollar against nearly all its major peers.

Japanese Yen: The Yen was the week's worst performer. The combination of strong U.S. economic data (reducing the need for safe-haven assets) and the widening interest rate differential between the U.S. and Japan made selling the JPY to buy the higher-yielding USD a dominant trade.

Euro: The Euro weakened considerably against the dollar, with the EUR/USD pair falling throughout the week .The strong U.S. data contrasted with the more fragile economic outlook in the Eurozone, reinforcing expectations that the European Central Bank may have to ease policy sooner than the Fed.

British Pound & Canadian Dollar: In a notable divergence, the Pound and the Canadian Dollar were remarkably resilient against the dollar's rally. Both currencies ended the week nearly flat against the USD. Their stability suggests that strong domestic factors ,such as stable oil prices supporting the CAD or UK-specific economic news bolstering the GBP, were sufficient to counteract the powerful pull of the surging U.S. dollar.

AUD, NZD, CHF- The risk-sensitive Australian and New Zealand Dollars weakened as capital flowed toward the U.S. The safe-haven Swiss Franc also lost ground as the strong data reduced demand for defensive assets.

FINAL THOUGHTS

The past week was defined by a powerful divergence: while U.S. stock markets celebrated a perfect storm of positive catalysts, the global policy landscape grew increasingly tense and unpredictable. Now, attention pivots from last week's triumphs to the immediate challenges ahead. The July 9 tariff deadline will be a critical test of the administration's new trade doctrine and could trigger significant volatility.

Content on this site is for informational purposes only and does not constitute investment advice or a solicitation to buy or sell any financial instruments. MetaMacro makes no guarantees regarding the accuracy or completeness of the information provided. Unauthorized use, redistribution, or access to proprietary content is strictly prohibited. All information is subject to change without notice. Investments involve risk, including the potential loss of principal.

— Oghenetega

MetaMacro