Market Color | Midweek Motion- June 18, 2025

Market Turmoil as Geopolitical Storm Gathers; Economic Signals Mixed

Hello Metamacro readers! Top of the morning to you

Yesterday's trading session was dominated by a potent cocktail of escalating geopolitical tensions, particularly in the Middle East, which sent investors scurrying for safety and rattled equity markets worldwide. Meanwhile, a mixed bag of economic data offered little clear direction, further clouding the outlook. With central banks across the globe under scrutiny and a looming threat of heightened trade protectionism.

USD Gains Ground Amid Rising Mideast Tensions; Oil Jumps on Conflict Fears

The U.S. Dollar strengthened during the American trading session as worries mounted over potential U.S. participation in the escalating Israel-Iran conflict. This concern intensified following a meeting between President Trump and his national security team, coupled with Israeli Prime Minister Netanyahu's suggestion that U.S. military engagement could commence within days. The elevated geopolitical risk also provided a significant boost to crude oil prices, with WTI crude settling $3 higher at $73.27, reaching its highest closing level since late January.

Yields Fall on Safety Bid; Gold Ignores Mideast Jitters

In a classic "flight to safety" move, U.S. Treasury yields declined, indicating increased demand for government bonds. The 10-year yield fell 7 basis points to 4.385%, and the 30-year yield retreated from the 5.00% mark to 4.88%. Surprisingly, gold did not exhibit its usual safe-haven behavior despite the geopolitical tensions, trading nearly unchanged around the $3,383 level.

US Economy Offers Mixed Picture: Weak Retail Sales Countered by Stronger Core and Industrial Data

On the economic data front, the U.S. delivered a mixed bag of signals. Retail sales for the month came in weaker than anticipated, declining by 0.9% against a forecasted 0.7% drop. Core retail sales, excluding automobiles, also fell short of expectations, registering a 0.3% decrease compared to the predicted 0.1% gain. However, a key bright spot emerged from the control group, a direct input into GDP calculations, which surprisingly rose by 0.4%, surpassing the 0.3% estimate.

Additional economic reports presented a varied picture. Both industrial production and capacity utilization proved stronger than forecast, and the NAHB housing market index showed a modest improvement. Meanwhile, business inventories aligned with expectations. Overall, the day concluded with a blend of economic signals amidst increasing geopolitical uncertainty.

First Export Decline Since Sept 2024 Adds Pressure on Japan's Economy

On the data front, Japan's exports experienced their first year-on-year decline since September 2024 in May, intensifying concerns about a potential technical recession following the negative GDP growth recorded in the first quarter. Exports decreased by 1.7% compared to the previous year, primarily due to weaker performance in the automotive, steel, and mineral fuels sectors. While still a contraction, this figure was better than the anticipated 3.7% drop. Meanwhile, imports saw a more significant fall of 7.7%, driven by reduced shipments of crude oil and coal.

Trump Exits G7 with UK Deal, Signals Tough Stance on Japan and EU Trade

President Trump concluded his G7 participation after securing a trade deal with UK Prime Minister Keir Starmer, declaring it "signed and done." However, his departure was marked by hints of stiff resistance on other trade fronts. Trump stated Tuesday that Japan was proving "tough" in ongoing trade discussions and that the European Union had yet to offer a "fair deal." He also reiterated his intent to soon send a "take it or leave it" letter to Japan. Adding to trade tensions, Trump warned that pharmaceutical tariffs are "coming very soon." Meanwhile, US trade talks with Canadian Prime Minister Mark Carney are also under close scrutiny this week, with Trump acknowledging "different concepts" needing resolution.

Gas & Auto Declines Drag Down May Retail Sales Beyond Forecasts

U.S. retail sales experienced an unexpected decline in May, primarily due to reduced spending on gasoline and automobiles, marking the second month impacted by President Trump's widespread tariffs. Headline retail sales fell by 0.9% for the month, exceeding economists' forecast of a 0.6% decline. This downturn was significantly influenced by a 2% drop in gasoline sales, a substantial 3.5% slide in auto purchases, and a 2.7% decrease in building materials. Conversely, miscellaneous store retailers saw the largest increase in May, with sales rising by 2.9%.

Walmart Nears Record Losing Streak as Shares Slide for 10th Straight Session

Shares of Walmart were trading marginally lower on Tuesday, marking what could be their tenth consecutive session of declines. This potential losing streak would tie the company's longest slide in its price history dating back to 1972. Notably, Walmart's stock has only experienced a ten-day losing streak twice before: once in 1980 and again in 2004. This extended downturn puts the retail giant's stock performance under the spotlight.

Economic Calendar

The Bank of Japan has already announced its decision, maintaining interest rates at 0.4%-0.5% after its two-day policy review. The focus now shifts to the Federal Reserve, which is set to announce its interest rate decision later today, Wednesday, June 18, 2025.

Adding to the economic landscape, U.S. retail sales for May came in weaker than anticipated, declining by 0.9% against a forecasted 0.7% drop. This suggests a potential slowdown in consumer spending.

Looking ahead to the rest of the week, the Bank of England is scheduled to announce its interest rate decision on Thursday, June 19, 2025. Investors will also be watching for the release of the UK CPI report on Wednesday, June 18, 2025, which will provide crucial insights into UK inflation, and US unemployment claims also on Wednesday, June 18, 2025.

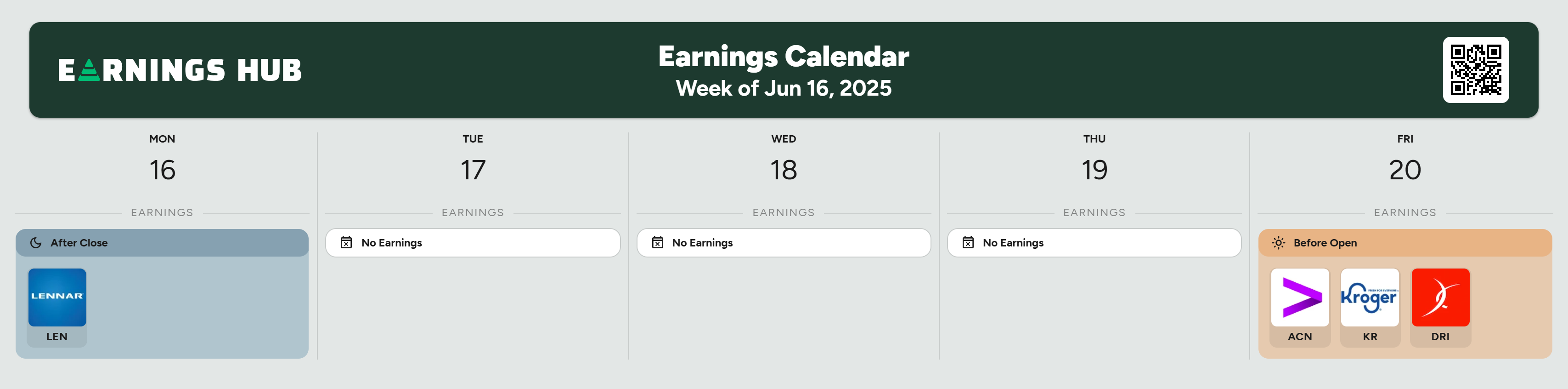

Earning Calendar

Lennar Corporation released its Second Quarter Fiscal 2025 earnings with a mixed performance, with revenue exceeding expectations but missing profit targets. We still expect earning earnings report from Accenture Plc, Kroger and Darden Restaurants on Friday.

Equities Color

S&P 500 Index(SPX)

On Tuesday, the S&P 500 index experienced a downturn, settling at 5982.05 compared to its preceding close of 6033.11. This decline was largely attributable to heightened geopolitical tensions surrounding potential U.S. intervention in the Israel-Iran conflict.

Dow Jones Industrial Average Index(DJI)

The Dow Jones Industrial Average experienced a considerable downturn yesterday, concluding the session at 42,209.89, a decrease from its previous close of 42,515.09. This movement primarily stemmed from an increase in risk aversion, influenced by prevailing geopolitical tensions, a varied domestic economic landscape, and persistent uncertainties regarding international trade.

US 100 Index(NDQ)

Consistent with the S&P 500 and Dow, the Nasdaq Composite experienced a downturn, settling at 19,519.47 compared to its prior close of 19,701.21. This movement was primarily driven by heightened concerns regarding potential U.S. participation in the Israel-Iran conflict, which prompted a divestment from growth-oriented technology equities.

FX SNAPSHOT

The USD generally gained strength against most major currencies yesterday driven primarily by safe-haven demand amidst escalating geopolitical tensions in the Middle East and mixed US economic data.

FINAL THOUGHTS

The market currently feels like a tightrope walk over an abyss of uncertainty. While geopolitical tensions cast a long shadow, driving investors to defensive positions, the underlying economic data presents a complex and fragmented narrative. The coming days, particularly with central bank decisions and crucial inflation data, will be pivotal in shaping the immediate market direction.

Content on this site is for informational purposes only and does not constitute investment advice or a solicitation to buy or sell any financial instruments. MetaMacro makes no guarantees regarding the accuracy or completeness of the information provided. Unauthorized use, redistribution, or access to proprietary content is strictly prohibited. All information is subject to change without notice. Investments involve risk, including the potential loss of principal.

— Oghenetega

MetaMacro